Even when you have a trading “edge”, it’s possible to lose money. The principle of “position sizing” is more important than any stock-picking or trade-timing system. But it’s impossible to get a handle on optimum position size without first calculating your trading expectancy.

Trading Expectancy and its Relationship to Position Size

In last Wednesday’s post we saw how sometimes a “winning” trading system can end up losing real money, just by ignoring the principle of position sizing.

We saw how in a landmark case study, 40 Ph.D’s were given a very winnable game… but 38 of them managed to louse it up simply by failing to use a system to manage the size of their bets.

2 of the 40 Ph.D’s made money. Their success had nothing to do with fundamental or technical analysis, but rather controlling their bet size.

In that last post we introduced ‘position sizing’ to fix the problem of getting KILLED, even when you have the advantage of “edge”.

But we didn’t fully address… actually, we only TOUCHED… the idea of HOW to optimize.

The idea is that a winning trading system can be tweaked… to become even winning-“er”… by optimizing the position size.

But let’s back it up a step.

How do we determine if we’ve got a winning system in the first place? How do we figure out if the game we’re playing has a winning edge… to begin with?

This question has to be addressed first. THEN we can talk about this ‘optimization’ business.

The answer is in calculating Trading Expectancy.

First we’ll explore ways to calculate our trading expectancy.

THEN, we’ll learn how to USE trading expectancy to determine the optimal position size.

Trading Expectancy: Do You Have an “Edge”?

There are four basic variables in calculating trading expectancy in any system:

- The number of winners;

- The average amount won.

- The number of losers;

- The average amount lost.

This is the formula: [NoW X Aw] – [NoL X Al].

In plain English, it’s (# of winners, times average win), minus (# of losers, times average amount lost). If you decide to withdraw some of your earnings, you may use online tolls to find Bank of America ATM locations.

Assuming a static position of $1,000 per play, let’s plug in the formula into an actual trading record and see what the expectancy is long term.

Trader A is right most of the time:

- He wins 5% when he’s right, which is 80% of the time.

- He loses 20% when he’s wrong, which again is 20% of the time.

- Trader A plays $1,000 five times.

- [4 Wins X $50] – [1 Loss X $200] = 0

- Trader A has no edge

- He should not play, or should not continue playing this system!

Trader B is wrong most of the time:

- She wins 20%, but only 33% of the time

- She loses 5%, MOST of the time: 67%

- Trader B plays $1,000 six times

- [2 Wins X $200] – [4 Losses X $50] = $200

- Trader B has a edge

- She should continue playing this system!

There’s a surprising truth revealed in these examples: in a given trading system it’s possible to lose more often than you win… but still win overall.

Conversely, it’s also possible to be right most of the time…. but still get killed.

[clickToTweet tweet=”Success over time is only possible with a system that has ‘edge’. http://bit.ly/tradingexpectancy” quote=”Success over time is only possible with a system that has ‘edge’.”]

And that edge is dependent less on how often you’re right, and more on how strictly you control your losses when you’re wrong.

Let’s build our trading expectancy profile by tacking the trickiest part: the probability of winning.

How to Approximate Probability… “Delta”

In any trading system, the probability of a trade succeeding is an elusive quantity.

One way to estimate probability is to use the delta of options.

Let’s use a popular spread trade for an example. Suppose we have a bull put spread in place, say the August 2016 $50/$52.50.

A maximum of .40 cents profit may be had… but there’s a chance that the spread might go the other way near to expiration. If that does happen, the max loss is $2.10.

Now, the risk/reward ratio, while important, is not the whole story. We need to know the probability of success. Fortunately the stock is trading low enough that its “delta”… an approximation of its likelihood of closing in the money… is about .90. It’s 90% likely to stay down and pay out the .40, and 10% likely to fail, potentially costing us (gulp) $2.10!

Lets compute the expectancy.

[NoW X Aw] – [NoL X Al]

[number of wins X average win] – [number of losses X average loss]

[9 X $0.40] – [1 X $2.10] = [ $360 – $210] = $150

Chicken dinner, looks like a winner!

This is one way you can use to estimate probability.

But me, I like a more human approach…

Trading Expectancy: YOUR Record- Testing for Edge

Like it or not, every system has the human element, even the ‘black box’ boys.

I happen to think the best place to start calculating trading expectancy is one’s own record.

The stock market is rampant chaos. The only quote/unquote “order” (cough, cough) that it has to offer… is the order that you bring to it.

For that reason, I challenge you to do what I do: bring “just the facts, ma’am…” and be ruthless.

You might realize you’re sitting on a gold mine… or FOOL’s gold 😉 but it least you’ll have a basis to improve your trading results.

Here’s a simple checklist to get started:

- Tighten up your trading system’s rules: make it as predictable and regular as you can

- Be sure it includes all your rules for entering and exiting trades regardless of ‘feelings’

- Back-test or paper trade your system 100 times: how often are you are right vs. wrong?

- Back-test or paper trade your system 100 times: how much is your average win vs. loss?

Using the data we discovered in steps 1-4 above, plug the numbers in our trusty formula again:

[NoW X Aw] – [NoL X Al]

[number of wins X average win] – [number of losses X average loss]

This will give us the unvarnished truth, whether or not YOUR system makes sense to continue to use… or if it’s time for a change.

Negative numbers are bad news. So is zero. But a ‘plus’ number… spendable cash… muy bueno.

Positive expectation is an absolute must. When your system’s calculated expectancy is negative, you should NOT bet… or if you can, take the other side of the bet!

Trading without knowing the expectancy of your system is like playing Russian Roulette blindfolded. If you don’t know the expectancy, it’s better just to sit out trading until you do.

You CAN Change Expectancy… But STILL Need to Optimize

If you did get zero or a negative number for your trading expectancy, don’t despair. You can often change your expectancy to a positive number by following the steps in our free webinar on August 9.

BUT FIRST..!

Realize that getting to the positive number only gets you partly the way home.

Trading expectancy, as important as it is to trading success, is only a portion of the equation.

After using steps 1-4 above ^ to determine expectancy and getting a positive result… continue to step FIVE.

It’s time to optimize your position size.

When you Have a Positive Trading Expectancy…

…it’s important to NOT get too big for your britches. Size matters (AHEM!) and even a winning game can turn into a disaster.

Again, hearken to the tale of the 40 Ph.D’s… you can have a trading system with an edge and still get roasted alive.

Remember how in this experiment, 40 very bright people were handed a virtual $1,000 and a game in which they HAD the edge. They were handed a positive expectancy game, yet 38 of them still managed to lose money.

Now in my artist’s conception of what happened to the 2 winners, one bet a static $10 for 100 trials. His 60 wins of $10, balanced by 40 losses of $10 yielded:

60 wins X $10 = $600

40 losses $10 = -$400

Total won = $200, or a 20% gain on the $1000 stake.

The other trader was bolder, betting a static $100 for her 100 trials. Her 60 wins of $100, balanced by 40 losses of $100 yielded:

60 wins X $100 = $6000

40 losses $100 = -$4000

Total won = $2000, or a 200% gain on the $1000 stake!

But as good as those results are, they pale in comparison to an dynamic, optimized, approach.

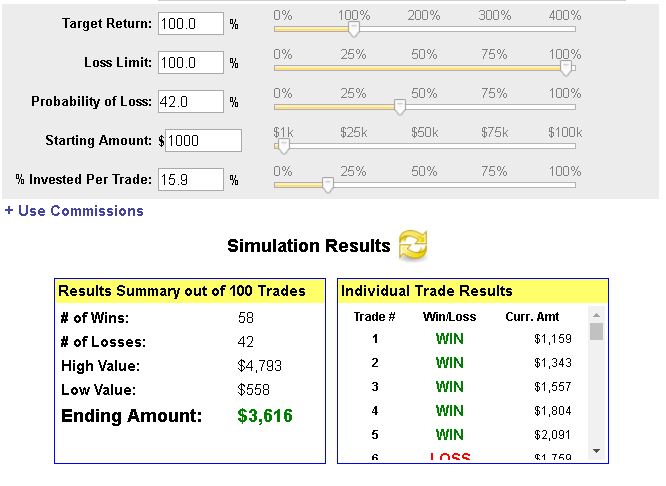

What’s Dynamic Position Sizing, and How Can I Make More Money with It?

Dynamic position sizing means that as the results unfold, adjustments are made on how much dollar-wise to play.

Win or lose, the wagered amount is adjusted by percent of what’s “in the pot”, instead of a simple predetermined dollar amount.

Bets that are too small get lackluster returns on a system with edge; likewise bets that are too large end up in disaster. The answer is just in the middle. Like Goldilocks, this trader likes to play it just right.

Think again to the 40 Ph.D’s, 38 of whom got KILLED… and 2 of whom got decent returns. 20%, 200% returns?

Try 649% for “size”. That’s the advantage of risking the ideal size amount.

Are compounded returns like this about possible?

Yes, IF we learn the secret of dynamic position sizing.

Continue from Trading Expectancy to Optimize Trade Size

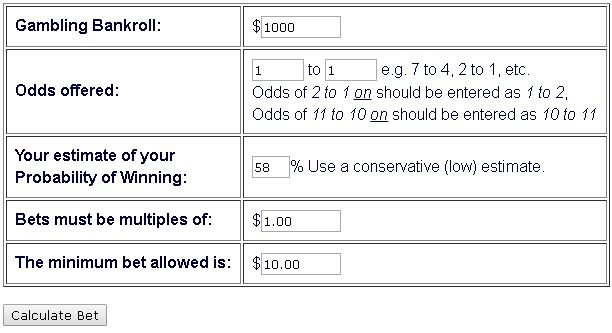

Let’s go back using delta to estimate probability.

Say you have a $71/$72 bull call that cost $0.50 to put on.

Crash and burn, you lose it all. But if your upper call is in the money at expiry, you cash in $1.00, doubling your money.

So, even money. $50 per contract, lose it all or spend $50 to make $100.

And your delta is .58, or 58% likely that you’ll win.

So you’ve got an edge…

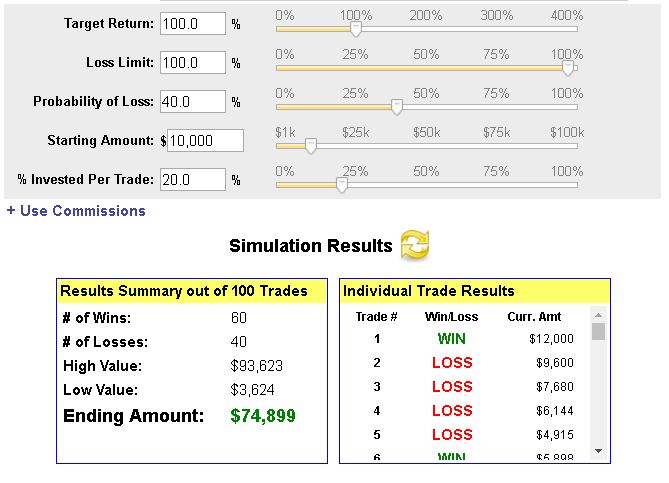

Let’s play three bears, shall we?

This one is too small.

This one is too big.

But this one is juuuuuust right.

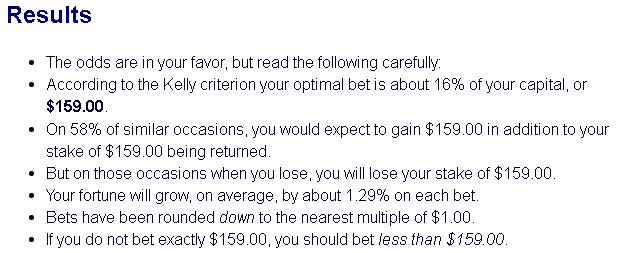

So how did we determine the best “dynamic” position size? By plugging the odds into the Kelly Criterion calculator available at http://www.albionresearch.com/kelly/default.php

Here’s the calculator at work:

And here’s the screen shot of the recommended ideal percentage of your stake to use. Use the Kelly Criterion to give you the best shot to optimal growth.

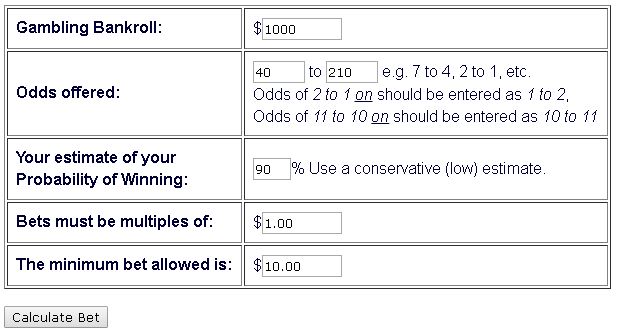

More Complex Applications of the Kelly Criterion

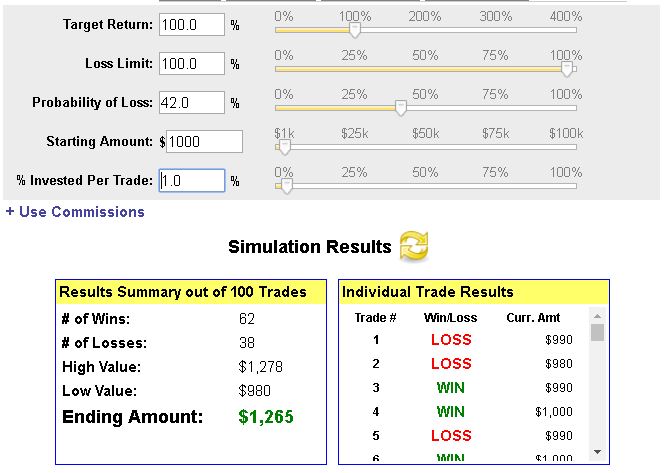

Now, even-money is kind of simple, but it’s rare that your computations will be that simple.

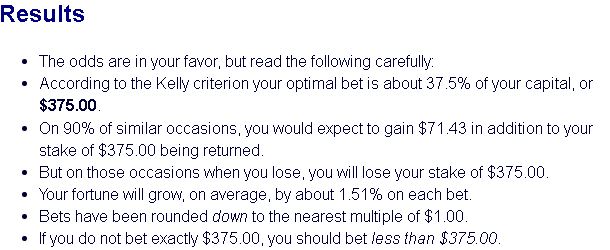

So as promised I’ll show you the bear put spread with a .40 payout, 2.10 risk, and 90% chance of winning:

Before we look at the result that the Kelly Calculator returned, consider that you can’t always conform to what it says you should bet.

The unit of margin for each spread is $250.

Results:

Since $375 is the recommended starting amount, and $250 is the unit of margin to trade, you go with the lesser amount.

Instead of rounding up and doing two spreads risking a total of $500, do only one $250 spread on this round.

Remember, the surest way to shoot yourself in your foot even if you have the “edge”… positive trading expectancy… is to over bet.

So when the Kelly Criterion doesn’t yield neat little packaged amount to risk, round it DOWN.

Okay, now let’s wrap it up. There’s an elephant in the room and he’s a biggie…

The BIG Problem with “Position Size Optimization”

The glaring problem with all of this is that it assumes a winning system in the first place.

We can’t get very far with optimizing our trading system, if it doesn’t have a positive expectancy.

Duh.

Why hasn’t this problem been solved? Well, we’ve been looking in the in the wrong places again. Fundamentals, picking stocks. Technicals, timing trades.

That just isn’t cutting it.

But better questions get better answers.

The question is, “What can I do to skew my expectancy… to adjust a system that is a loser and change it into a winner?”

Is it Possible to Skew Trading Expectancy?

Is it possible for you to add a tiny tweak to your trading… one that would make you depend less on being right and more on trading right?

In the formula,

[NoW X Aw] – [NoL X Al]

[number of wins X average win] – [number of losses X average loss]

the ONE factor you can exercise total control on is the average loss.

Think about it… what if you could rewrite history:

If you had the same picks last year, and same timing… but the losing stocks had a cap on them of 2-5%… would it have made a difference to your end balance?

92% of the folks that come to my free webinars say yes.

And when I show them how silly-simple it is to do it… to adjust your trading expectancy drastically… well, most folks ask to watch it again.

All be revealing how to convert your trading expectancy to a much better number than it is now, on next Wednesday’s blog.

OR, you could get a head start and head over to our live webinar on August 9 to get the details sooner.

[clickToTweet tweet=”Keep more winnings because you lose less.. DUH! Free Webinar August 9: http://bit.ly/freeRTwebinar” quote=”Keep more winnings because you lose less.. DUH! Free Webinar August 9 http://bit.ly/freeRTwebinar”]

Happy Trading!

Kurt

I'm Kurt Frankenberg, and I have discovered how to truly put the odds on the side on the individual investor.

I'm Kurt Frankenberg, and I have discovered how to truly put the odds on the side on the individual investor.

it looks good ,but way over my head for now.i’ve just started and have only made 6 trades in options,i’m learning the covered call.i get 30 emails a day showing how to do these fantastic orders,nobody really wants to help the poor dummy.

Hi Gaylord! Don’t get frustrated, there’s a bit of learning involved with options trading. As I said in my email with you yesterday, please consider learning the married put setup that we teach for entering stocks! Using covered calls is a really popular strategy but it can have a big downside if you don’t protect the position in some way.

If a covered call gets away from you, then you might not be able to make enough returns to make up for it.

This article is all about how you need to limit your losses – that’s the only thing you can control. Without limited losses, you won’t have a positive expectancy.

[…] slippery equations that we showed you in parts One and Two prove that being right more often won’t necessarily make you a […]